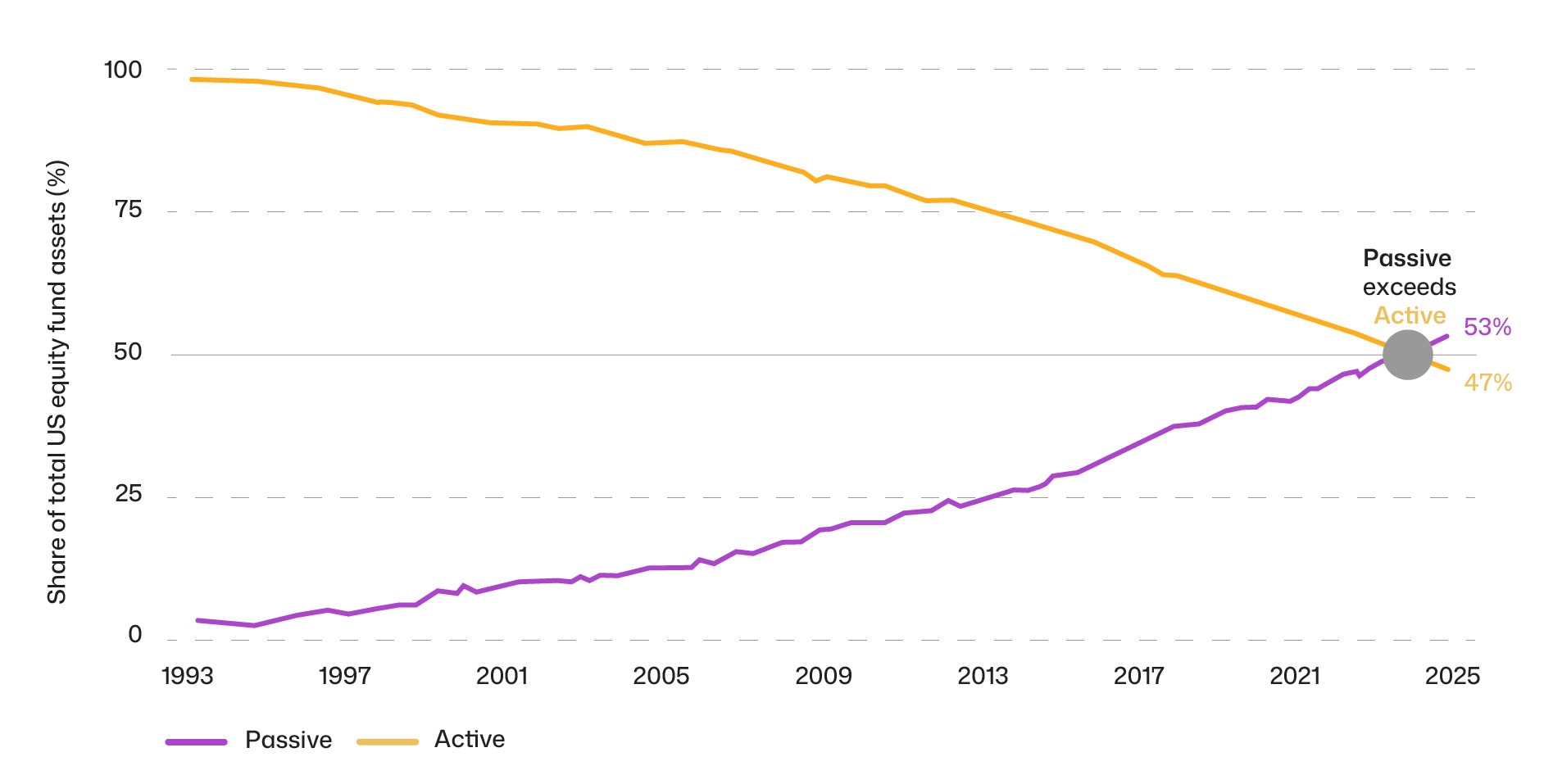

This rise in passive investing has made markets more accessible to everyday investors, but it has also sparked debate over its wider effects on capital allocation, price discovery, and overall market stability.

Although it continues to deliver lower costs and more resilient fund flows, there’s argument that it can also distort stock valuations, increase volatility, and create inefficiencies with broader economic consequences.

Passive is not truly passive: inflows, redemptions, index changes, and rebalancing trigger mechanical buying and selling that can move prices significantly, rendering it algorithmic, reflexive, and pro-cyclical.

Large flows buy or sell baskets of stocks simultaneously, amplifying swings and synchronising movements. As passive investing grows, price discovery weakens. Fewer active participants evaluate fundamentals, increasing the risk of sharper corrections.

Maybe this mattered less when passive funds were a small share of the market, but because of its rise, we think passive investing may expose investors and equity markets to a range of risks.

Active investors analyse fundamentals to establish fair valuations, but passive strategies accept current prices. As passive flows grow, fewer participants assess companies’ true worth, arguably weakening market efficiency and leading to potentially sharper corrections when mispricings become recognised.

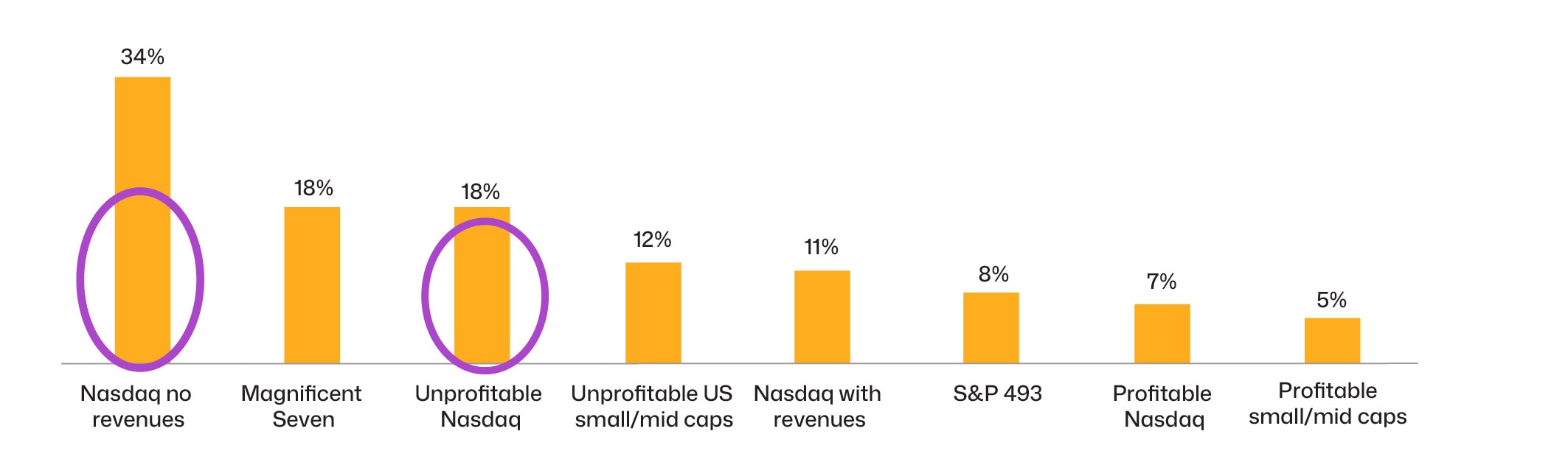

Market-cap weighting funnels capital to already-rising stocks, risking overvaluation and deep reversals. Research indicates that around 10% of current market volatility derives from the growth of passive investing, with high-passive-ownership stocks showing 2-3x flow sensitivity.8

Passive funds are indifferent to company valuations and so they buy large-caps indiscriminately, causing prices to move in unison across sectors and this, we believe, erodes diversification benefits.

Indices skew heavily toward a few giants and passive replication channels disproportionate funds there, masking concentrated risk as broad exposure and tying market performance to a handful of names.

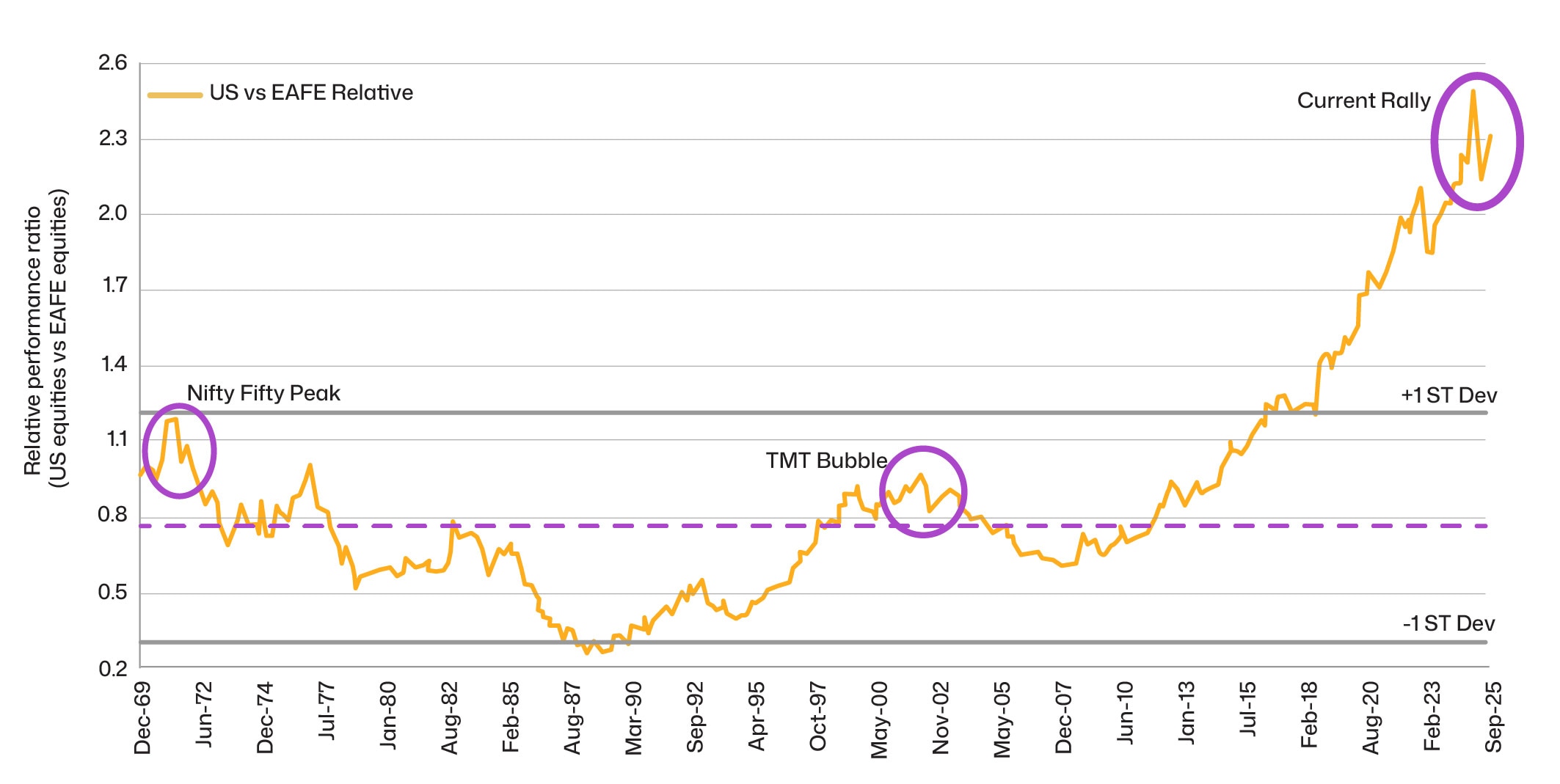

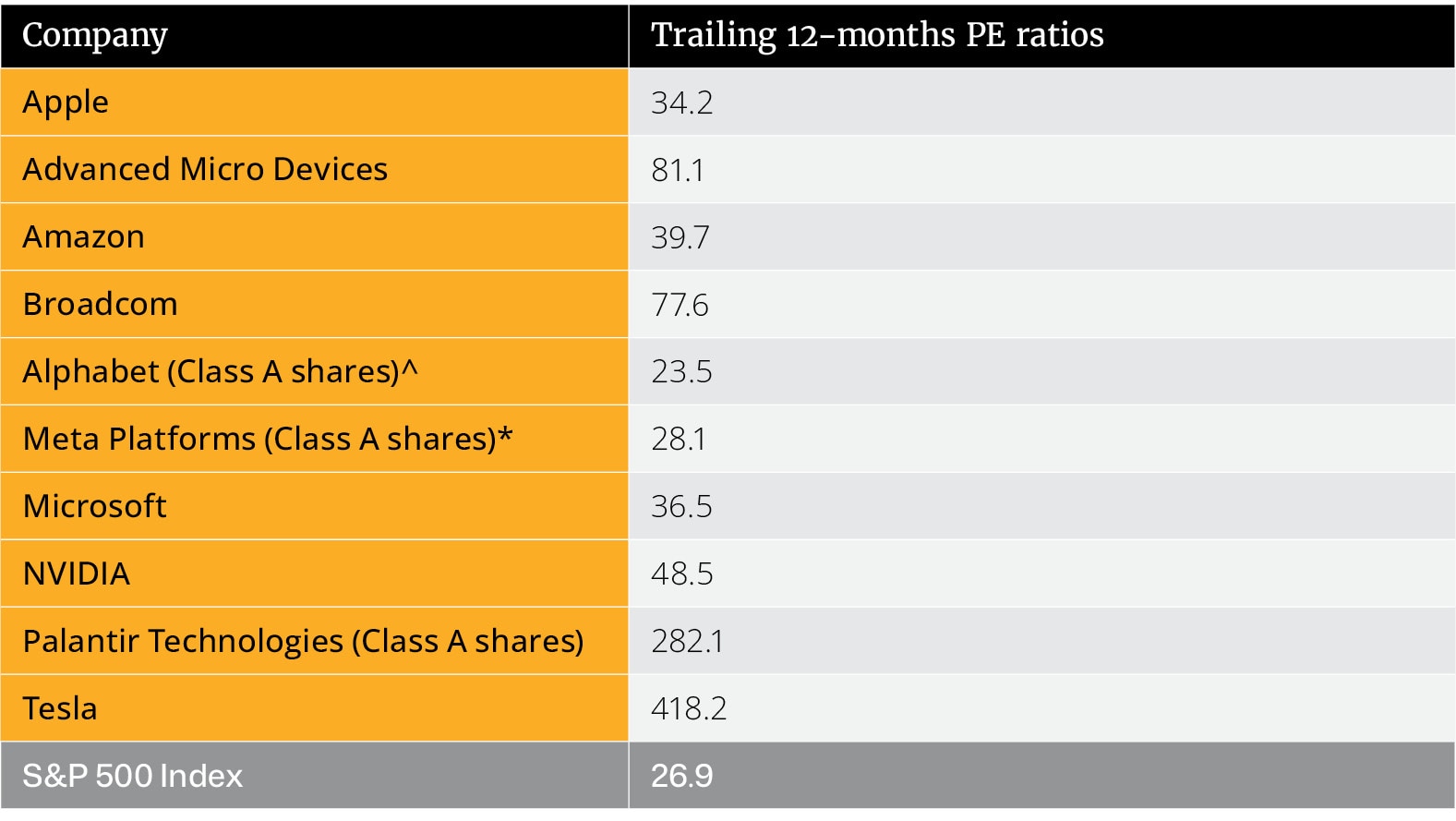

The S&P 500 Index is a case in point: The Magnificent Seven — Apple, NVIDIA, Microsoft, Amazon, Tesla, Alphabet, and Meta — together comprised around 33% of the S&P 500 Index’s market capitalisation during 2025 but accounted for 42.5% of the Index’s total return (in US dollars).9

Indices were originally neutral tools, ways to measure and track market performance. Today, they can be said to actively drive it.

Arguably, the surge in passive investing has transformed major indices like the S&P 500 and MSCI World from passive reference points into major forces that allocate capital across markets. In effect, indices themselves now function as some of the most influential participants in the market, effectively blurring the traditional distinction between passive and active investing.

For both retail and institutional investors, passive strategies remain a cornerstone due to their low costs and broad diversification. However, heavy reliance on them increases the risk of sharper drawdowns in highly concentrated markets. In more volatile environments, active management can become more attractive, particularly by focusing on under-owned stocks to reduce concentration risk.

The final word on passive investing should appropriately go to Vanguard’s founder, John Bogle, who asserted: “If everybody indexed, the only word you could use is chaos, catastrophe… The markets would fail”.10

Prospects for active managers’ performance rebound

Predicting turning points is fraught and often humbling, as American baseball legend, Yogi Berra, famously observed in one of his many memorable quips: “It’s tough to make predictions, especially about the future”.

One potential catalyst could be disappointing returns on massive capital outlays by technology companies. The AI boom is driving enormous demand for computing power, prompting firms to pour billions into infrastructure.

McKinsey estimates that global data centre spending could reach US$6.7 trillion by 2030 to meet this surge in compute needs.11 This stunning figure exceeds the Gross Domestic Product (GDP) of all countries bar the US and China.

Historical capital expenditure (capex) booms offer sobering lessons, as detailed in an October 2025 research paper12 that examined major investment cycles — railroads (1860s–1890s), late-1990s telecom fibre, and the current AI surge — measuring them relative to GDP and tracking leading company shareholder returns.

It also observed that the Magnificent Seven are shifting from asset-light models toward capital-intensive operations.

A clear pattern emerged: firms that aggressively expanded their balance sheets underperformed more conservative peers by an average of 8.4% per year from 1963 to 2025.13 This “asset-growth anomaly” persisted across 10 market sectors studied; multiple geographic regions (US, Europe, Asia); both boom and bust periods, and various forms of capital spending.14

Rapid capex growth companies showed similar weakness, most acute in the dot-com bust but persistent otherwise.

Today’s AI-related spending already exceeds the internet boom’s peak relative to GDP. When adjusted for shorter AI chip lifespans compared with traditional infrastructure, current levels surpass even the 1860s–1870s railroad expansion era.15

Big technology companies were estimated to have spent nearly US$400 billion in 2025 alone,16 with AI capex contributing roughly half of US GDP growth.17 Justifying this scale would require generating around US$2 trillion in annual AI revenue by 2030, yet current AI revenues are only around US$20 billion, implying the need for a 100-fold increase.18

On this analysis, today’s technology behemoths have very steep bars to clear to justify their immense capital commitments. If returns disappoint, valuations face risk, potentially favouring lagging sectors and stocks where active managers maintain conviction.

Benefits of diversification evident in our portfolios

A scan of our global share holdings shows investments in the likes of Microsoft, Apple, Nvidia, and Alphabet, capturing some upside, though at moderated weights.

To us, this is just one example of the merits of diversification as the complementary styles and philosophies one of one manager are balanced by those of another. Headwinds for our active global share managers have been ameliorated, to some extent, by smart beata and passive strategies.

Our active equity managers are uncovering more stock-specific opportunities in Europe and the UK, including companies benefiting from higher structural defence spending, offsetting US caution.

Options strategies developed and implemented by our highly capable in-house derivatives team has enabled us to benefit from the rise of technology stocks without the lags and costs associated with owing physical stocks. Hedging the Australian dollar has also meant that our members’ and clients’ global investments have been cushioned from the local currency’s rise.

Investments uncorrelated with share markets — like Insurance Linked Securities where institutional investors can invest in securities that transfer the financial risk of large natural disasters from insurers and reinsurers to capital markets — too have been important sources of return as well as portfolio diversification.

Other alternative investments, such as those related to legal and government receivables, have also been valuable sources of returns as well as diversification from public market risks.

In Australian shares, we believe the strong run from mid-cap and small-cap resources stocks means that the relative opportunity in industrials is looking more encouraging over a three-to-five-year earnings horizon.

Our conviction in diversification, proven across cycles, remains firm.