Australia’s economic performance

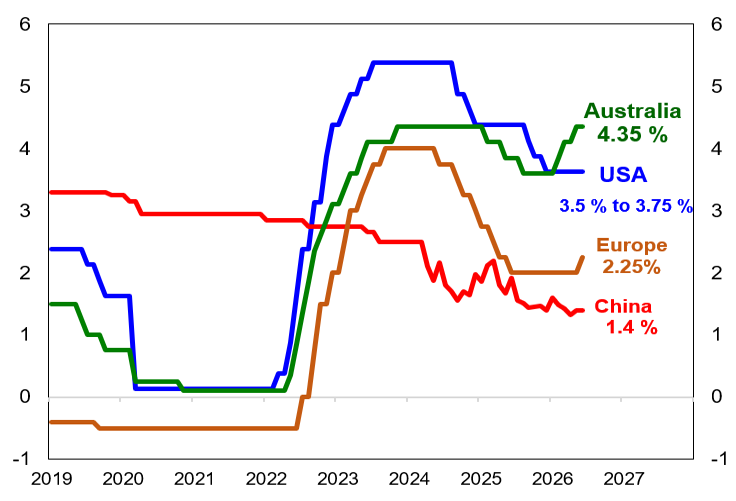

Australia’s economy is slowing down judging by the modest economic growth of only 0.3% for the March quarter and 2.5% for the past year. The economy is becoming more dependent on AI investment in building data centres and government spending to keep the lights on. The recovery in consumer spending after the RBA’s interest rate cuts last year is now fading. The three interest rate rises in 2026 and high inflation are placing enormous pressure on consumers’ budgets. While the RBA held interest rates steady in June 2026, the central bank did warn that it is prepared to raise the “cash rate target further if required”.

Notably business and consumer confidence have been registering weak results in recent surveys. The Federal Government’s announcement of major changes to capital gains tax and negative gearing in May has also cast a shadow over prospects for the residential property market. Australian house prices have started to fall led by sharp declines in Sydney and Melbourne. While the Federal Government did extend the fuel excise tax cut until the end of July, the price benefit has been reduced from thirty-two cents to sixteen cents per litre. Hence for many Australian consumers, the “cost of living” squeeze is continuing.

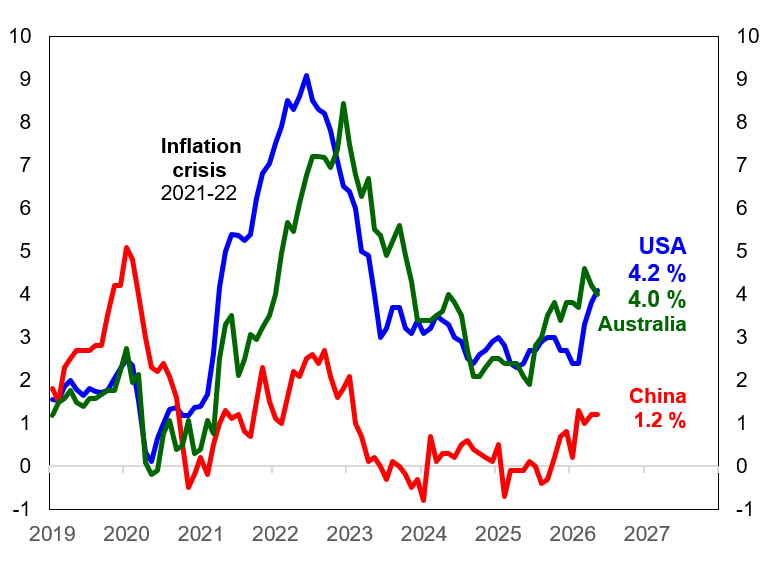

Fortunately, Australia’s labour market has been stable with mild jobs growth and a steady unemployment rate around 4.3%. Wages growth at 3.3% has also been solid in the past year although this has been below the current 4% inflation rate. There is a good chance that the Australian economy can still muddle through this tough patch of slower economic growth and high inflation without further interest rate rises. However, our resilience is likely to be further tested by the precarious climate of global politics.

Global prospects

While financial markets are now hopeful that the ceasefire between Iran and the US will eventually end the war, the military and political situation remains volatile. Leaders in the US, Israel and Iran still need to compromise to ensure that the current ‘Memorandum of Understanding’ becomes a formal peace agreement. Regrettably, there is still a chasm in trust between the warring parties. Until a formal agreement is signed and the drones and missiles stop flying, financial markets and commodity prices remain vulnerable.

If the Iran War intensifies again, this would be a severe challenge for the global economy. Both inflation and unemployment could dramatically rise. For central banks around the world this creates a major policy dilemma – should central banks raise interest rates to restrain inflation pressures or lower interest rates to assist economic activity and mitigate rising unemployment.

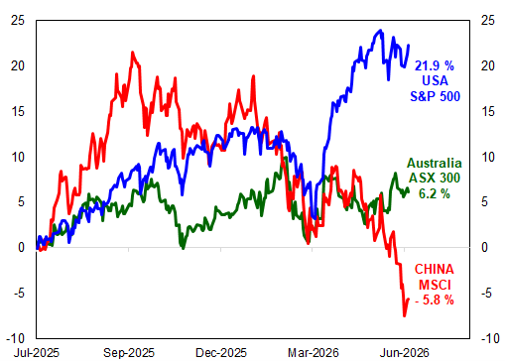

Regrettably, the RBA has been a pioneer in raising interest rates three times this year. The European and Japanese central banks also raised interest rates in June. If other major central banks such as the US Federal Reserve follow suit with interest rate rises, this could challenge the recent strong performance of global share prices.

Australian consumers are still being challenged by persistent inflation. Price pressures in food, health and housing are squeezing budgets. This continuing “cost of living” squeeze is likely to weigh heavily on consumer spending over coming months. Lower house prices will also caution some consumers on their spending.

Given these complex and significant risks, investors should maintain a disciplined and diversified strategy.